.svg)

This post argues that after fintech solved how money moves, the next infrastructure gap is how orders move safely. Social commerce already has discovery, chat, payments, and riders, but buyers still fear paying blindly and sellers still fear sending before payment. PickSpot solves this by giving buyers a delivery identity that connects order requests, safe payment, rider coordination, tracking, handoff confirmation, and merchant payout.

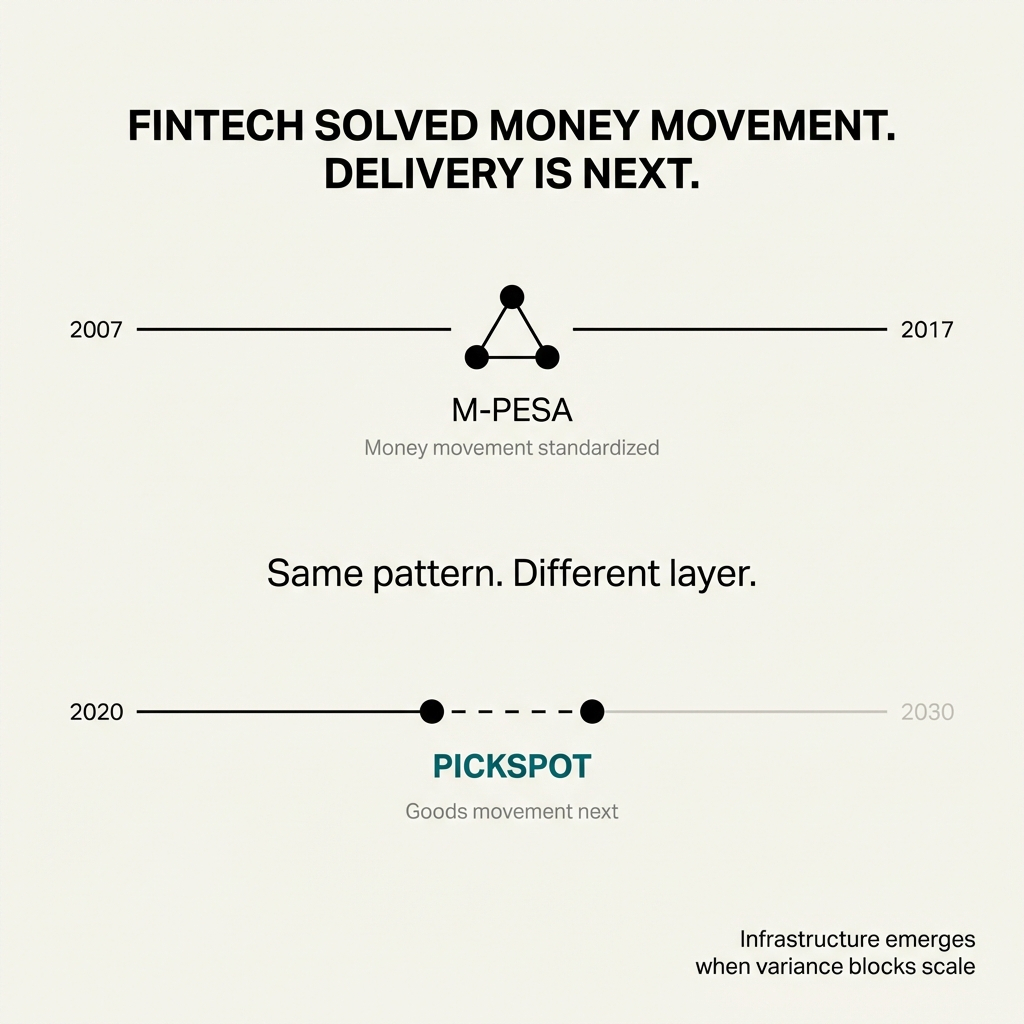

Fintech changed how money moves.

In Kenya, that shift is obvious.

A phone number became enough to send money.

Mobile money made payment instant.

Digital wallets made financial access more portable.

Small businesses could collect from customers without needing a bank branch.

Money got infrastructure.

But commerce is not finished when money moves.

An order still has to reach the customer.

And that is where the next infrastructure gap begins.

Social commerce already works at the top of the funnel.

Instagram creates demand.

TikTok drives discovery.

WhatsApp closes the conversation.

Mobile money moves funds.

Riders move parcels.

But the actual transaction still breaks in the middle.

The seller asks:

“Where should I send it?”

The customer sends a pin, a landmark, a building name, and extra directions.

Then the seller asks for payment.

The customer hesitates.

The seller hesitates too.

The buyer does not want to pay blindly.

The seller does not want to send before payment.

The rider needs clear delivery instructions.

Everyone is waiting for someone else to take the first risk.

That is not a payments problem.

It is a delivery infrastructure problem.

Before mobile money, sending money required coordination.

Who are you sending to?

What account should receive it?

Is this the right person?

How does the money reach them?

Mobile money gave people a simple answer.

The phone number became the identity that routed the transaction.

That identity made the payment feel normal, fast, and safe enough to repeat.

Delivery now needs the same kind of identity layer.

A PickSpot is that identity.

Something like:

It is not a pickup point.

It is not a location.

It is a private delivery identity connected to the customer’s saved address.

When a customer buys from a seller, they share their PickSpot. The seller uses it to send a proper order request through PickSend.

The customer reviews the product amount, delivery fee, and total cost.

They approve and pay.

PickSpot coordinates the rider.

The item is collected from the seller and delivered to the customer’s saved home address.

The customer tracks the delivery and confirms handoff.

The seller gets paid after successful delivery.

That is the missing layer.

Not just payment.

Not just delivery.

The infrastructure that connects identity, payment, dispatch, tracking, and handoff.

Fintech was not only about moving money.

It was about reducing risk.

A good payment system tells both sides:

The payer is real.

The recipient is identified.

The transaction has a record.

The money moved.

The system knows what happened.

Delivery needs the same structure.

A good commerce delivery system should tell both sides:

The buyer is real.

The seller sent a proper request.

The customer approved the total cost.

Payment happened before dispatch.

The rider was coordinated.

The parcel was tracked.

Handoff was confirmed.

The seller was paid after successful delivery.

That is why delivery infrastructure is becoming as important as fintech infrastructure.

Because commerce needs more than a way to pay.

It needs a safe way to complete the order.

Closed platforms already solved this inside their own walls.

Glovo, Jumia, Amazon, and Uber Eats give buyers structured checkout, saved delivery details, tracking, and proof of delivery.

But they also control the marketplace.

Social sellers do not want to give up the customer relationship.

They already have customers on Instagram, TikTok, and WhatsApp.

They do not need another closed platform.

They need platform-grade safety outside one.

That is the opportunity.

PickSpot gives open commerce the safety and visibility people expect from platforms, without forcing sellers into a marketplace.

Africa did not wait for traditional banking to reach everyone before building the future of payments.

Mobile money skipped a generation of banking infrastructure.

Commerce can do the same with delivery.

Many sellers will never build full checkout systems.

Many buyers will keep discovering products in chat.

Many orders will keep starting outside marketplaces.

Riders will remain distributed.

Addresses will remain inconsistent.

Trust will remain local and fragile.

That does not mean commerce cannot scale.

It means commerce needs a new layer.

A delivery identity layer.

A safe payment layer.

A coordinated dispatch layer.

A proof of handoff layer.

That is what PickSpot is building.

The first wave made people reachable by phone.

The second wave made people reachable by money.

The next wave makes people reachable by commerce.

Not by exposing their private home address.

Not by explaining landmarks every time.

Not by trusting strangers blindly.

But through one delivery identity that can start a safe order flow.

A PickSpot lets a buyer say:

“Send it to my PickSpot.”

And behind that simple sentence, the system can handle the hard parts:

Order request.

Payment.

Rider coordination.

Tracking.

Handoff.

Merchant payout.

That is why delivery infrastructure is the next fintech.

Because once payments are solved, the next question is obvious:

How does the order safely reach the person who paid?